Create marketing funnels in minutes!

Your page? Unpause your account to remove this banner.

Learn more

Sign Up To Get The Full Course Right Now!

Yes, I am ready to get started today!

* we will not spam, rent, or sell your information... *

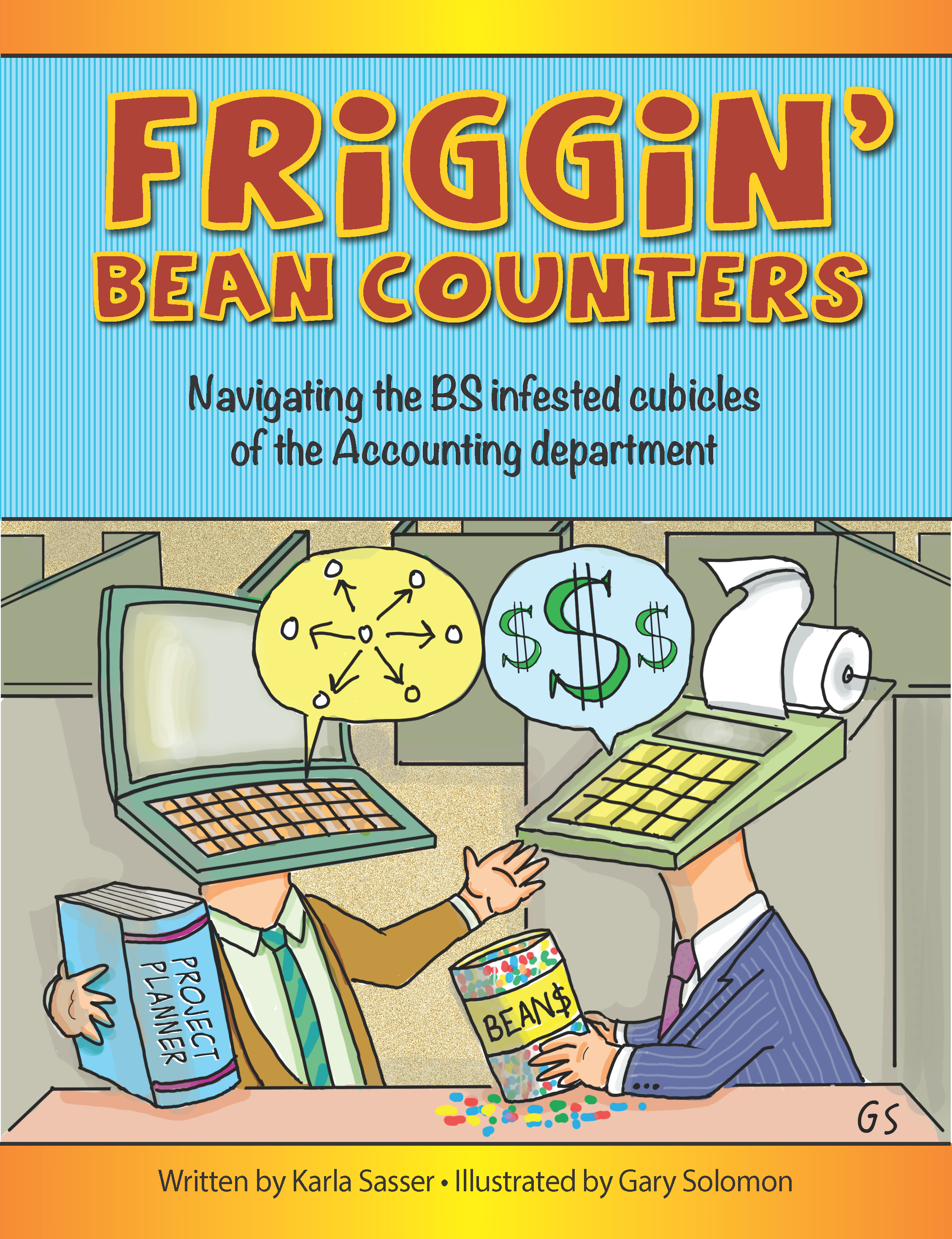

IT and Project Management Failing?

The Solution is HERE

Enter your email for a FREE download of the KEY

Download Article

Submit and Check your inbox for your free link to view article!

Facebook

Twitter

Google+

Facebook

Twitter

Google+

KSasserPL, Copyright 2017 All Rights Reserved

Working...